Can anyone post this article here

The Indian textile and apparel market is looking at an unlikely and short-lived opportunity to gain global dominance. It remains to be seen if the stakeholders can come together and do what is required.

economictimes.indiatimes.com

The Indian army is well aware of a two-front challenge at its borders. India Inc is now staring at a two-front opportunity.

India’s

textile and apparel market (T&A), estimated at over $99 billion in 2021-22, has a chance to use this opportunity to grow its exports. The country's T&A exports were $33.5 billion in 2019-20 and $44.4 billion in 2021-22, according to the Ministry of Commerce. The segment is expected to reach $65 billion by 2025-26, growing at a CAGR of 11%, according to an analysis by Wazir Advisors based on the Directorate General of Commercial Intelligence and Statistics’ data. The promising segment now has a chance to grow further because of several disruptions in

China and

Pakistan — major T&A suppliers to the world.

China grows about 20% of the world’s cotton. But most of its major customers have restricted purchases because of allegations of human rights violations and labour issues. Major economies have banned cotton from Xinjiang — accounting for 84% of China’s cotton exports — for a year now. Pakistan, also a key competitor in the textile and apparel segment, has been affected because of floods. Nearly 40% of the cotton crops have been damaged, say government sources. The country, with a large informal manufacturing base, has also been facing a nationwide power crisis, leading to huge spikes in raw material prices and the cost of production. These factors have stalled global supplies from these destinations and major importers are now looking at other options. This is where India has a chance.

To put things in perspective, industry experts say the impact of the flood in Pakistan on India’s export orders will be limited to the current export season. Indian apparel exporters are sitting on a strong order pipeline for the current export season — the spring-summer season extending from September 2022 to May 2023 — according to

MVIRDC World Trade Center Mumbai. “One reason for the strong order pipeline is the adoption of the China +1 strategy by global apparel buyers, which led to the shifting of export orders to India. But the industry is wary of predicting the growth outlook for world textile exports due to recessionary concerns in USA and Europe and also because of the natural gas crisis in Europe,” says Vijay Kalantri, Chairman of the trade facilitating organisation. He estimates the annual global textile and apparel export size at $901 billion.

Size of the opportunity

However, India can replace China and Pakistan as global suppliers in 248 commodities across the textile value chain — right from fibres to readymade garments — according to experts at the MVIRDC World Trade Center. “The USA, Japan, the UK, Australia, Malaysia, Vietnam, Togo, Nigeria, Benin and The Gambia are the potential export markets for these goods as China and Pakistan largely cater to these markets. Some of these products are women’s dresses of synthetic fibres, terry towels, women’s tracksuits of man-made fibres, polyester yarn, cotton babies’ garments, cotton fabrics, carpets and floor coverings and cotton bed linen,” says Kalantri.

India has a competitive edge in these products because it already has over 5% share in the global export of these goods. So, there is a lot of growth potential in these goods.

A research report by the MVIRDC states China and Pakistan export over $60 billion worth of these 248 products annually. “China itself exports $52 billion. India’s number is hardly $27 billion, not even 50% of the total export of China and Pakistan. Therefore, there is untapped export potential for India in these 248 products,” it adds.

The annual global export value of these 248 textile and apparel products is $209 billion or 23% of total textile and apparel exports as of 2021, according to the Geneva-based International Trade Centre (

ITC

). China remains the largest exporter with a 25% share. India comes next with 13% for these 248 products. Other major exporters such as Turkey, Vietnam and Bangladesh have 4% share.

Narendra Goenka, Chairman of the

apparel Export Promotion Council (AEPC), says there is a potential business opportunity for India. However, India might not make an immediate gain due to recessionary pressures in major textile importing destinations. “After March-April 2023, we expect some visible changes favouring the country,” he adds.

Demand dampener

The question is, what would it take for the industry to capitalise on this opportunity? Several things have to fall into place. For one, the industry needs some support from the government and favourable weather to ensure there is adequate output of cotton, the primary source of raw material for textile production.

There are too many “unpredictable factors,” here, experts point out. These can include crop output, change in raw material prices and government policies, says Ronak Chiripal, Chief Executive Officer of textile firm Nandan Terry. “If everything goes well, Indian players will surely benefit from this shift. However, right now, global demand has reduced drastically in the textile market. If the market sentiment doesn’t improve in the next couple of months, the situation will become very tough for us,” Chiripal says.

The reference to cotton output is for the current year, 2022-23 and the cotton crop has already hit the market, and the volatility of unpredictable rain has subsided to some extent.

The

Russia-Ukraine war is giving the industry sleepless nights. “People are rather saving for the winter (because of rising energy prices in Europe and economic uncertainties) than spending on textiles and apparel. The demand situation must improve. Otherwise, forget benefitting from the new opportunity, we will also face huge losses,” adds the CEO of the Ahmedabad-based textile firm.

But if everything works out well, Chiripal estimates the company can gain 15-20% more in the next financial year.

As of now, there is 10-15% fluctuation in demand for cotton. It is gradually stabilising, says Mayank Tiwari, founder of digital ecosystem for natural fibre ReshaMandi.

Structural issues

The country’s MSME firms in this segment expect a significant change in demand patterns. They are hoping it will turn the tide as the textile industry has been in a terrible phase ever since yarn prices went on a rising spiral a few months ago.

But the fortunes of Indian firms won't change overnight because of these disruptions in China and Pakistan, says Vikas Singh Chauhan, Director at MSME-dominated Home Textile Exporters Welfare Association (HEWA).

The structural issues on the domestic front are too many and cannot be solved in a hurry. Chauhan points out that even if MSME firms get orders, they will have to deal with the high cost of packaging material in India. Basic equipment such as a bar coding machine is still not available with many players. “It takes 1-2 months to dispatch just samples.”

In India, modernisation has to happen on a large scale and at a fast pace for companies to be able to match China’s scale of operations. “Our pricing and quality are good, but their timeline is far better. While they dispatch goods within 25 days, we take 60-90 days. Our labelling and packaging are still not up to the mark,” says Chauhan.

Besides, he says, it is not feasible for any party to snap trade ties overnight because of some disruptions that can be temporary. So, buyers are unlikely to go for an alternative vendor from India just because the market in China and Pakistan isn’t good. “We need to give them something extra to persuade them to make the switch,” he says.

A pricing challenge

The HEWA Director says he had come across some buyers from the UAE who were looking to switch from Pakistan and China to India. But Indian firms’ “non-adherence to timelines” put the deal off.

Even Karur-based textile firm Aarthia Impex is getting similar inquiries from US buyers who source from China. But pricing issues stand in the way, says Prakash P, manager of the firm. “Despite cotton prices falling now, there is a 10% price difference in our and Chinese supplier’s quotes. if we get the packing and other costs streamlined, then we can grab these orders in 2023,” he says, adding he keeps very narrow margins but it all boils down to a 10% price gap that hurts suppliers like him. “One buyer mentioned that container costs are also high from Indian ports when compared with our counterparts. Buyers are astute. They compare all these aspects before moving their sourcing to another country,” adds Prakash.

Industry officials say any strategy for out competing China and others must also include a policy direction of not helping them. Because, repeatedly, these markets are seen to have grown at the cost of India’s raw material supplies.

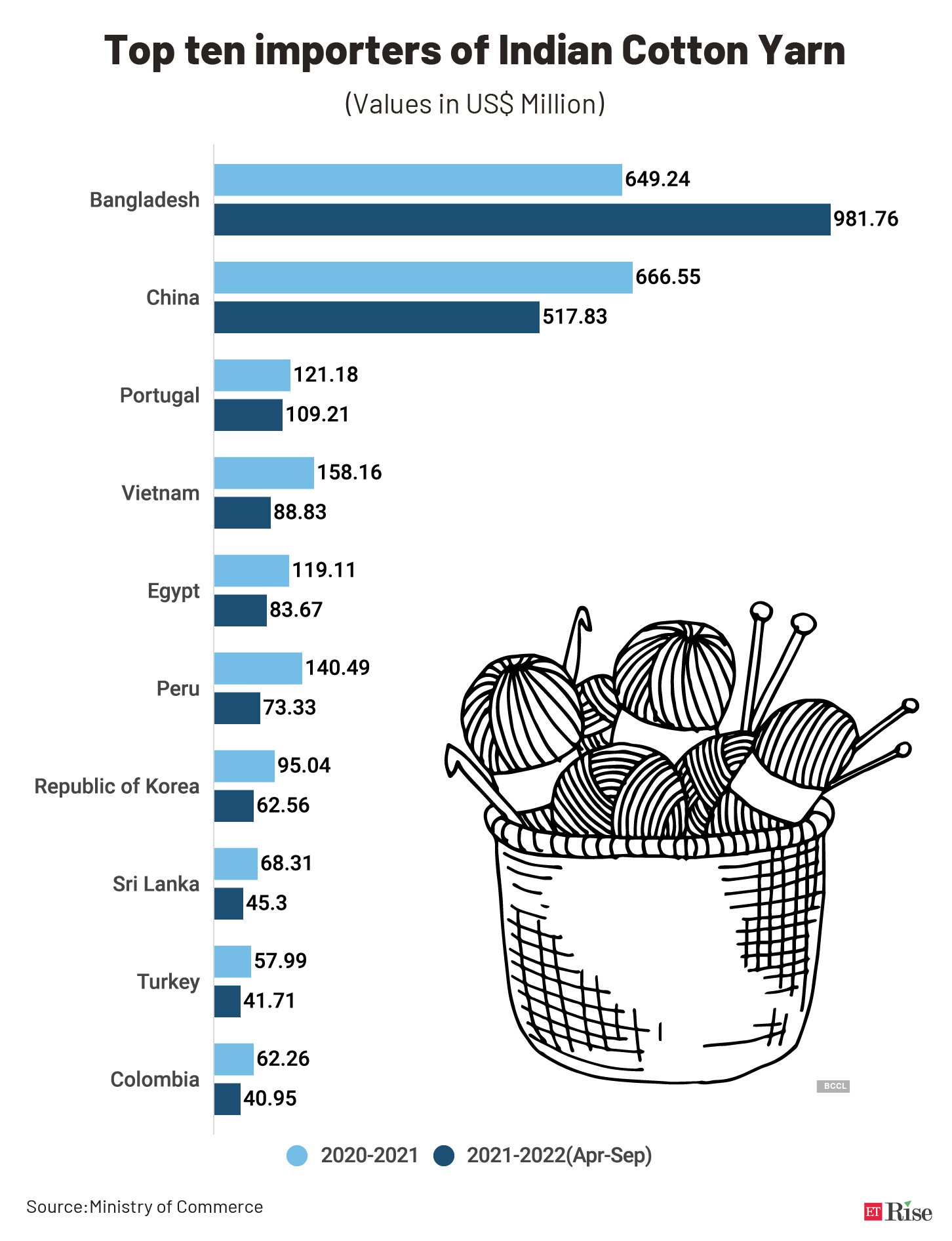

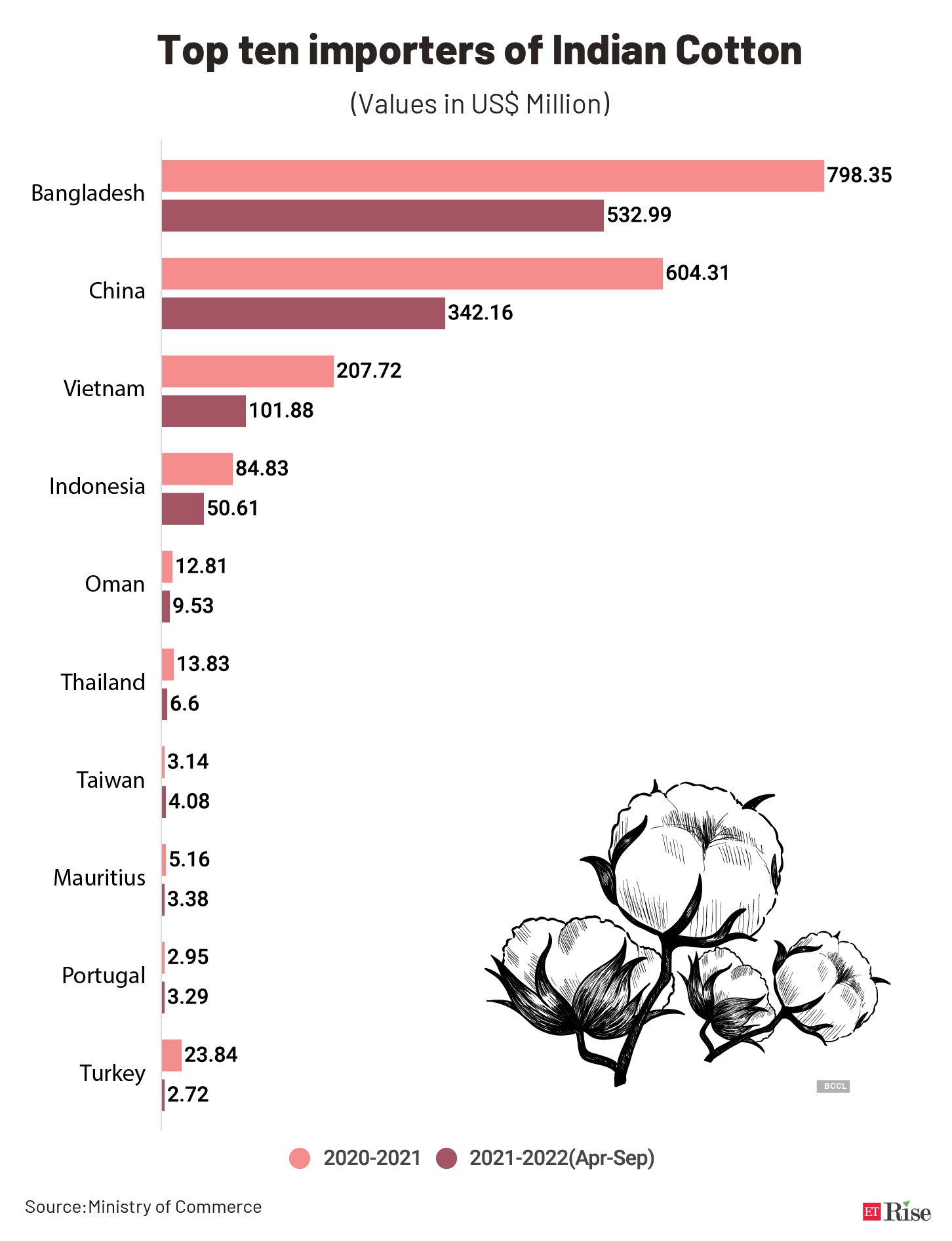

Consider this: India grows its own cotton, but the irony is that despite a big ban on Chinese cotton-based products, our players have not aggressively stepped in to fill that gap. “Because, throughout this year, we allowed rampant export of cotton and cotton yarn. We were busy exporting cotton and cotton yarn to fill in the gap created by the Xinjiang ban. Now, countries like Bangladesh always knew they could reduce their Chinese dependence and import cotton yarn from India. China is smart too. It's a net exporter of cotton yarn and garments. So we need to revisit our policies to push value-added exports,” says Gautam Nair, MD of Gurugram-based Matrix Clothing.

The challenges are conspicuous, so are the opportunities. Will someone take proactive steps to gain trade ground before the window closes?

Edited by Ram Mohan. Illustrations by Sadhana Saxena.

(Originally published on Oct 11, 2022, 09:43 AM IST)

m-economictimes-com.cdn.ampproject.org