Eight Charts: India Ascendant

By

Sloane Ortel,

Saurabh Mukherjea, CFA,

Vikas Khemani, CFA,

Sunil Singhania, CFAand

Navneet Munot, CFA

Posted In:

Economics,

Portfolio Management

India’s economy will experience the ordinary progress of a century over the next decade.

That sentence is as true now as it was in 1952 when Donald B. Macurda wrote of investment opportunities in India for

the CFA Institute Financial Analysts Journal.

The appeal was humanitarian, but also prophetic.

He wrote that the country “should logically become one of the world’s great steel centers,” and today it is. The prediction that “the Indian industrial ball will gather an accelerating momentum that could be enriching to all concerned” has also aged well.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

This is nothing if not an accelerating return.

This is because of pro-growth policy, not political personality.

India’s economic liberalization was really sparked

during a balance of payments crisis in 1991. Ten years later, the Asian Development Bank’s chief economist

observed that the need for continued work had become an item of widespread political consensus. To place the change in context, consider that the weighted average tariff on an imported product was 76% in 1990

according to the World Bank. It was 29% a decade later, and 6.2% in 2016.

That’s more a rebirth than a liberalization.

These compounding efforts have a straightforward result: India isn’t playing catch-up anymore. It’s the

world’s seventh-largest economy, and in some ways it’s already well ahead of “developed” places.

In early 2017,

Sloane Ortel estimated that a minimum wage earner in New York City spends 1.5% to 2.5% of their discretionary income on banking fees. In India, anything above 0% is an outlier. The

Pradhan Mantri Jan-Dhan Yojana (PMJDY, Scheme for People’s Wealth) provides not just free bank accounts to all citizens, but also free overdraft insurance. That makes capital formation easier, and it’s just one of a few hundred reasons why 8% GDP growth seems plausible for the next 20 years.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

Indian inflation has bottomed, and looks likely to rise further.

4:48 PM - May 30, 2018

So don’t be surprised if the economy starts running a little hot.

India’s inflation rate printed below 2% in the summer of 2017, but has since risen significantly. The

most recent release puts consumer prices up 4.58% from a year ago, and the year-on-year change has been well above the RBI’s target of 4% since November of last year.

The 1 July 2017 introduction of the national Goods and Services Tax (GST) is not least among its drivers. The 18% tax it collects on services is a significant hike from the 14.5% duty that was previously imposed on 28% of the CPI basket.

Fiscal policy is also likely to be accommodative until elections to India’s lower house of parliament, the Lok Sabha, in spring 2019. Local and national government social and infrastructure spending tends to spike in these pre-election periods.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

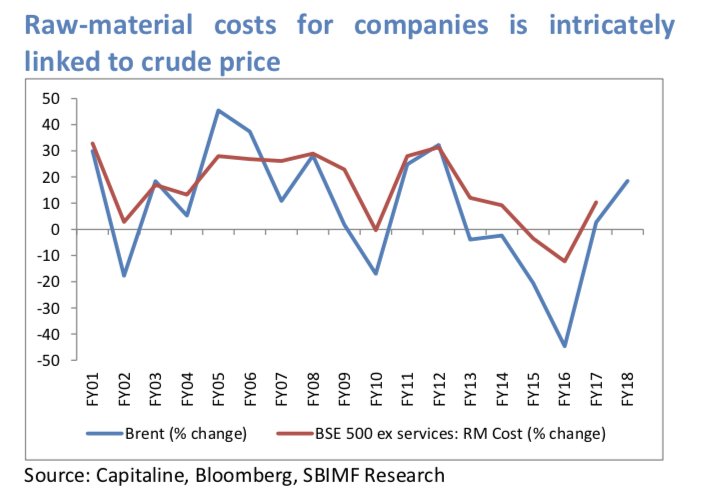

India's manufacturers face a crude reality.

4:52 PM - May 30, 2018

And of course, there are commodity prices.

India imports 86% of its crude oil requirement: about 1.5 billion barrels each year. That means rising crude prices have nearly a one-on-one impact on India’s import bill.

It’s less stark than it seems at first.

Refined petroleum is India’s largest single export. The country sent 207 million barrels abroad in 2016, making it the world’s fifth-largest supplier behind the Netherlands and netting $29.5 billion, 9% of the country’s total export trade.

For the Indian consumer, oil prices never fell. The government responded to the 2015 selloff by raising taxes on diesel and petrol. This increases reserves and can always be cut in the future. It’s also a footnote compared to some of the government’s other policy reforms.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

This is what an economic transformation looks like.

5:48 PM - May 30, 2018 ·

Brooklyn, NY

The informal sector accounts for roughly 40% of India’s 2017 output and employs almost 80% of its labor force.

The government seems determined to get rid of it.

India has digitized its financial plumbing, cracked down on cash, and issued a new national tax scheme largely to tamp out “black” money, or untaxed earnings on the black market. Many of these businesses are relatively low quality, and can be expected to lose share or cease operating without the ability to flout wage laws and avoid taxes.

This is a tailwind for listed companies. Market leading franchises have long been gaining share from these informal operators. Soon they will operate in a uniform national market with much less illicit competition.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

Indians are starting to discover their domestic capital markets.

5:52 PM - May 30, 2018 ·

Brooklyn, NY

The money habits of individual Indians are also headed for a significant change.

About 95% of India’s wealth is invested in physical assets: 77% in real estate with the balance in durable goods (7%), and gold (11%).

The remaining 5% is invested in financial assets. This share is already growing and looks set to go further. Households put 45% of their income into financial assets in 2012. The proportion is now around 58% and looks poised for more expanision.

This will materially strengthen India’s capital account if it continues.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

Not all borrowers pay their bills.

6:13 PM - May 30, 2018 ·

Brooklyn, NY

There are risks to the rosy outlook, of course.

A primary one is the sometimes lackluster credit discipline of Indian lenders. “India’s

bad loan/

twin balance-sheet problem is widely known and so far intractable,”

David Keohane wrote last year.

Historically, Indian companies have been weighed down by debt-laden balance sheets and the public sector banks that have financed them have been saddled with non-performing assets. In large part, this is because India’s bankruptcy code did not make it easy for creditors to reach economically viable arrangements. The Insolvency and Bankruptcy Code (IBC) of 2016 has materially strengthened the insolvency framework with an efficient legal structure to enforce debt service obligations.

It’s difficult to overstate the importance of this. The Asia Securities Industry and Financial Markets Association (ASIFMA)

estimated that India’s corporate bond market was worth about 15% of GDP in 2017. That’s tripled from 5% five years earlier, but is still much lower than neighboring Malaysia, where outstanding corporate bonds were worth 40% of GDP. Deepening this market will help to finance much-needed infrastructure projects and also provide banks with a bit more breathing room.

There are plenty of reasons to hope it works, but it may be a process. About two weeks ago, a Reuters headline blared, “

India State Banks’ Bailout Stumbles as Losses Mount.” And Moody’s

just cut their estimate for India’s 2018 GDP, citing a combination of higher oil prices and tighter financial conditions.

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

Accounting quality drives investment performance in India.

6:23 PM - May 30, 2018 ·

Brooklyn, NY

And then there’s the same old risk: Investing is hard.

Finding multibagger investments in India is a tricky affair because accounting quality and corporate governance standards vary wildly across companies and over 60% of the market cap of the frontline index, the NIFTY, is in highly regulated sectors like banks, telecoms, metals, power, infrastructure, and pharmaceuticals.

However, India had 5,615 listed companies in 2017,

according to the World Bank. That’s more than any other market on the planet: The United States had just 4,336. The top decile of these firms has historically delivered 10-times returns over 10-year horizons.

That’s a 25% compound annual growth rate. Foreign investors have participated in this growth story enthusiastically, which has kept India among the most expensive emerging markets based on trailing price/earnings multiples.

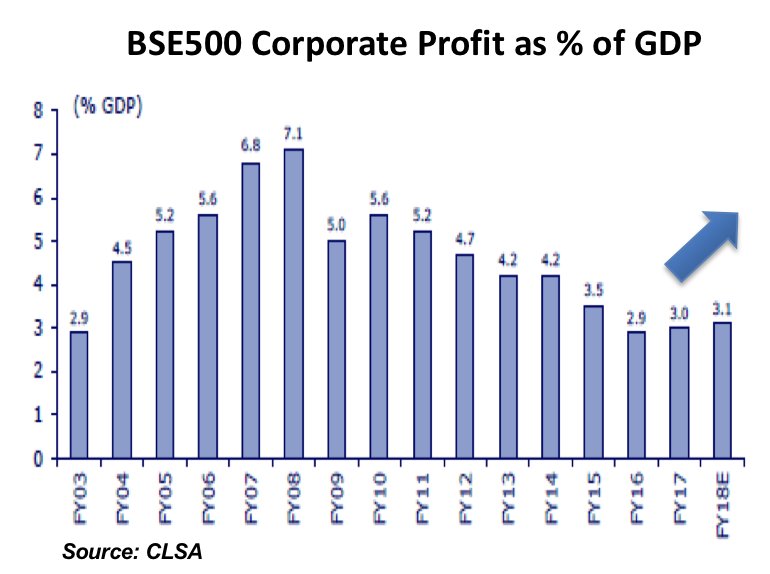

View image on Twitter

Sloane Ortel@sloaneortel

Sloane Ortel@sloaneortel

There's plenty of room for India's corporate profits to grow.

6:35 PM - May 30, 2018 ·

Brooklyn, NY

The standard question to ponder towards the conclusion of an article like this is: What inning are we in?

In India, though, the game is cricket, not baseball. One inning can last as long as four baseball games, and there are either two or four of them. The

longest game in historylasted nine days. And that’s really the point. An allocator encountering India today faces an unusual and alluring confluence of factors. The MSCI Emerging Markets Index

has only an 8.5% weighting to this fast-growing, cyclically attractive, and tailwind-laden economy.

The outlook is strong enough that we’ve gotten almost to the end before mentioning India’s

outrageously favorable demographics, swift digital rebirth, and booming middle class.

https://blogs.cfainstitute.org/investor/2018/06/05/eight-charts-india-ascendant/