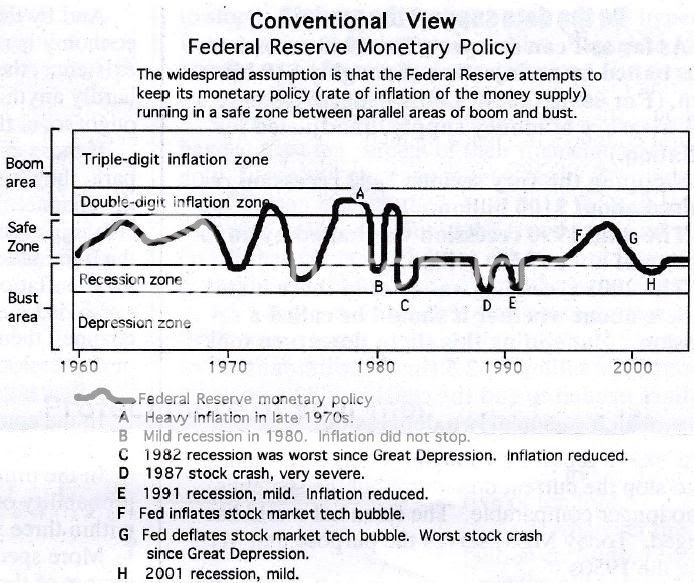

No, it's not. The train of thought is correct. That is exactly what we measure in long-run Solow and Harrod-Domar models- growth in steady-state.

Refer to the graphs in the link as you read this.

Neoclassical growth model - Wikipedia, the free encyclopedia

Note: We will be assuming a closed, no-trade economy and then contrasting it with an open, free-market economy to highlight just where the trend of thought diverges from the conclusion.

Also note, per-worker and per-capita are used interchangeably.

Before, we embark on this discussion, it is useful to know what a 'steady-state' is. The steady-state, in economics, is the state where increasing entropy of the resource-goods conversion has placed a limit on the amount of economic growth, so that it is no longer technologically, environmentally, ecologically or otherwise possible or feasible to increase production and for that reason, both consumption and population remain stable. This is a philosophical-sociological-ecological construct (the "carrying capacity of an organism) in economics and biology, and is one borne out of moral and ecological concerns and perceived limits to technology it is not an

actual physical or real constraint. But it is one with sound, if yet unproved, ground nevertheless.

Now in our neo-classical models elucidated in the the

wiki link, and among most economists and classical economic proponents of the limits-to-growth theory, steady-state

growth is assumed to be a linear growth that is a function of the rate of perceived technological progress and the rate of labor force (population) growth. The

rate of the steady-state growth, which is a long-run growth, and understood as the slope of the black line in the diagrams, is itself assumed to be a function of the change in capital in the long run (the capital replacement rate: which is a net of some function of the Savings rate and the rate of capital depreciation) aggregated by the number of workers. Since in the long-run, as seen in most Western countries, the population growth

rate slows to a small positive or to zero, it is not a key variable in the determination of steady-state growth. So, long-run steady state growth, is in current neo-classical economic understanding, determined principally by the all important rate of capital formation, or the net capital change or capital replacement rate, aggregated by the number of workers. In other words,

capital-per-worker change is the

key determinant of long-run growth. The net capital change per worker is measured as investment-per-worker minus the depreciation rate of capital (per worker) and is what we must remember as the key determinant of long-run growth in a steady-state (an economy near its carrying capacity) economy. We measure the growth rate: change in output-per-worker. Note that the black line in the graphs correlates output-per-worker (our measure for growth and the trend increase in "living standards") to capital-per-worker.

That's the demand-side.

The other side is the supply-side and its determinant: the investment per-capita, or

investment-per-worker, which translates into

capital-per-worker in the long-run. For our purposes, Savings=Investment, since, in a close economy with no inflation, savings translates directly into investment i.e. savings can only be invested locally, and whatever is saved is invested. This is indicated by the green, concave curves in the figure.

Note: how this assumption fails, when there is no closed economy or inflation. In an open economy, savings-per-capita may be higher or lower than Investment-per-capita: since Investments flow in or out- through domestic or foreign, institutional and direct investments. So,in an open-economy, savings-per-worker does not translate neatly into realized or

real capital-per-worker. Where high Inflation, on the other hand, or a steep growth in Money Supply comes in, Savings from one period does not translate directly into Investment in the next since inflation erodes the

real value of Investment: hence diminishes the

real capital-per-worker. It also discourages Savings itself, thereby reducing the Saving

rate or prompts an outflow of Savings and Investment. All this causes the green curve, in our figure, to have a considerably more concave shape.

That's the supply-side.

So, we've got two curves to help us determine our long-term, steady-state growth.

The green curve measures real capital-per-worker (Investment) as a function of savings-per-worker (Savings). And the black line correlates the real capital-per-worker (Investment) to output-per-worker (Growth). Of course, Growth is also assumed to be a function of the population growth rate, which we hold constant or zero, in the long-run.

Now, in the model or a closed-economy with no inflation, when the savings-per-worker or real investment-per-worker on the Green curve

exceeds the capital-per-worker on the black curve required in the steady-state: that capital-per-worker necessary to exactly offset capital depreciation and marginal population growth at the steady-state, there is a "capital deepening" effect- which is that there are positive, although diminishing, output returns to Capital. In other words, additional real capital-per-worker (Investment) brings in a higher real output-per-worker (Growth). So the savings rate per-worker, which is our vehicle for capital-per-worker, will, given that there are only a fixed number of workers at that point, increase till this "capital deepening" effect is completely exhausted in the short-run: to the point where there are no additional positive output returns to capital: viz. the steady-state- where capital-per-worker is just enough to offset the depreciation in capital and account for the steady-state output-to-capital returns of the small population growth, but no more.

So, in a closed economy with no technological change, that's what happens. Capital-per-worker, borne of savings and investment-per-worker and output-per-worker, borne of the

given state of technology, interact to give us a steady-state

rate of growth.

Now, what we call "technological growth" is simply an exogenous change through invention, innovation etc. in production methods that results in a one-time jump in output-per-worker, given the same level of capital-per-worker. In other words, for the same level of capital-per-worker, I can now produce at a certain higher level of output, given the same number of actual workers. Another way of understanding this is: that Technological growth has actually augmented the number of "effective workers" in my company, given a certain level of capital. To maintain a "steady-state" rate of growth then, which is that conceptual growth limit in the long-term, I would require a rate of technological growth, that would at least offset the

change in invested capital-per-effective worker with the

change in output-per-effective worker. In other words, the minimum level of technological growth needed to maintain long-run steady-state growth rate is that at which the output-per-effective worker exactly offsets the capital-per-effective worker invested.

The intuition underlying this is not hard to follow:

- If I were to consider 'n' as my population growth rate, and 'g' as my technological growth rate, then because Technology is augmenting capital-per-worker ( Capital/Worker -> K/L or simply 'k' ) and labor, L each new unit of worker entering the economy gives me a capital-per-effective worker of (n+g)k, where k: is capital-per-worker; because: 1) additional units of workers from population growth require Capital to be increased by n.K/L ('rate of population growth' x 'Capital per worker', K/L) for those workers to be of any use in the workforce; and 2) Technology, itself, is augmenting capital by g*K/L per worker ('rate of technological growth' x 'Capital per worker'). So my capital-per-effective worker with technological growth is: (n + g)k.

- To match this, I require an output that provides for a similar return of outpute- to-effective worker. No longer does my Output growth, at steady-state, only have to account for the rate of capital depreciation and population growth- it has to account for the new technology-augmented capital-per-effective worker as well [Remember: (n+g)k ] because, as you know, Capital also displaces Labour.

- The basic intuition is that, unless you replace worn-out Capital, provide each new worker entering the workforce with the same amt. of capital, and invest in capital to keep up with technology (the three conditions that our output under technology must achieve) then the level of output-per-effective worker falls despite the growth in invested capital per-effective worker. So, to achieve our steady-state level of growth, the level of output-per-effective worker, under technological change must at least be: (n+g+d)k, where d: rate of capital depreciation.

This is not so hard when you think of it: to warrant a given level of capital investment per worker, under technological change, I must achieve a level of output, that takes into consideration depreciation, population growth and the growth rate of technology (which simultaneously makes workers more effective, but displaces some as well) itself.

In our graph, a bump up of the technological growth rate, i.e. g, would be modelled as a pivot upward of the black line, since at every level of existing capital-per-effective worker, I can now at steady state, produce a higher, in fact 'the higher level required', of output per effective worker.

Now, this is in a closed economy with no foreign trade and no foreign investment, but with technological change. Imagine, an open-economy, where technology can be imported from abroad and investments made into foreign economies and vice-versa, so that higher capital creation-per worker could accrue from a given level of domestic saving and investment. This could accrue through current transfers, net positive receipts of interest on int'l investments, current transfers like remittances, portfolio holdings, loans and trade credits, increase in rupee reserves held by foreign countries or a range of other investment mechanisms. A key assumption of these neo-classical steady-state models is that capital is subject to diminishing returns in a closed economy. In fact, diminishing returns (the concavity of the green line) is exactly why we get a steady-state level of output that is lower than what it would be if, say we had constant or increasing returns to capital. Now, real returns on capital invested, or savings, are the nominal returns adjusted by the inflation rate. In a closed economy, invested capital reaches a saturation point (the steady-state line) beyond which the

real, inflation-adjusted output return to capital is

negative. That is, net investment, in real-terms, as capital-per-worker reaches its long-run equilibrium when it is equal to output-per-worker. But, in an open economy, where savings can be invested abroad, the

real returns to capital (the rate of nominal return on capital invested – my domestic inflation rate) don't have to be diminishing to the extent that they are in a closed economy. We have already seen why. U.S. investors in China in the 90's are an example: as opposed to the U.S, where investment retention probably have earned diminishing returns, U.S. investments in China in the 90's actually earned increasing returns. In fact, if enough markets are sought, the diminishing returns could be delayed for a

very long time. From a modular perspective, that would mean an adjustment of the concavity of the green line by making it

much less concave, pushing steady-state output and capital per-worker much higher. And we haven't even taken into account the effect of technological change yet! Exogenous (modelled outside the model) bumps in technology could, for the same level of capital invested-per-effective worker, push the output-per-effective worker ever higher (this is illustrated by a pivot upward of the black line) so that for all levels of capital-per-effective worker, in both short and long-runs, output-per-effective worker is higher.

Now, why was all this important? Because, while you have correctly identified the relation between inflation and growth in the short-run, the long-run growth determinant is actually

capital creation per-capita. So, while

high current and

expected inflation has everything to do with the impact of Savings on GDP growth through the Investment component of GDP: by diminishing the rate of Saving and through the exchange rate under the uncovered interest parity equilibrium. In the long-run because markets are free and because Saving can be invested abroad, domestic inflation does not bear the same relation with domestic capital creation - unless consistently high and that too, higher than the highest available nominal rate of return. On the other hand, a consistently

low rate of inflation, as has been the case in most Western economies for many decades now, and a low expected rate of inflation has exactly the opposite effect with respect to technological change: it acts as a catalyst for technological growth in the long-run in an environment where markets are highly developed, slight product differentiation is essential, competition is largely technique- or marketability-based and a large number of competitors in the market exist.

A little inflation (as in the case of most Western economies) is good for growth, because it is necessary to bring about the guarantee of price rise, that is necessary for long-term investment and adapting to technological change. Given a highly competitive economy, or one that is becoming highly competitive, an investor will be reluctant to invest unless he knows that prices are going to increase. That is because, given an exogenous technological bump, adopting the technology entails restructuring costs that the investor is unlikely to recover, unless prices rise in future. By making the production process more efficient: through Technological change in the productive process, I can increase profits in a competitive market, with stable market shares, only if prices are expected to increase. The expected price increase (expected inflation) is justified in a perfectly competitive economy only to the extent that it accounts for my restructuring and reinvestment costs. Consistently high inflation actually reduces my profits in the long-run to the extent that it impinges upon domestic Consumption- of also my goods. In the long-run, a low expected rate of inflation, by being positively correlated with the interest rate, provides a reason for foreign investment by increasing the Time Value of Money. A high inflation rate, of course, along with high expected rates of inflation prompt capital flights and a reduction in savings, investment and capital-per-worker. A low current and expected inflation rate also makes it viable for companies in developed markets to adapt to technological change, thus justifying the reason for the process itself.

Inflation and economic growth bear a non-linear relationship; there is a threshold beyond which there is a trade-off between growth and inflation. But below this a modicum of inflation is necessary to sustain growth.